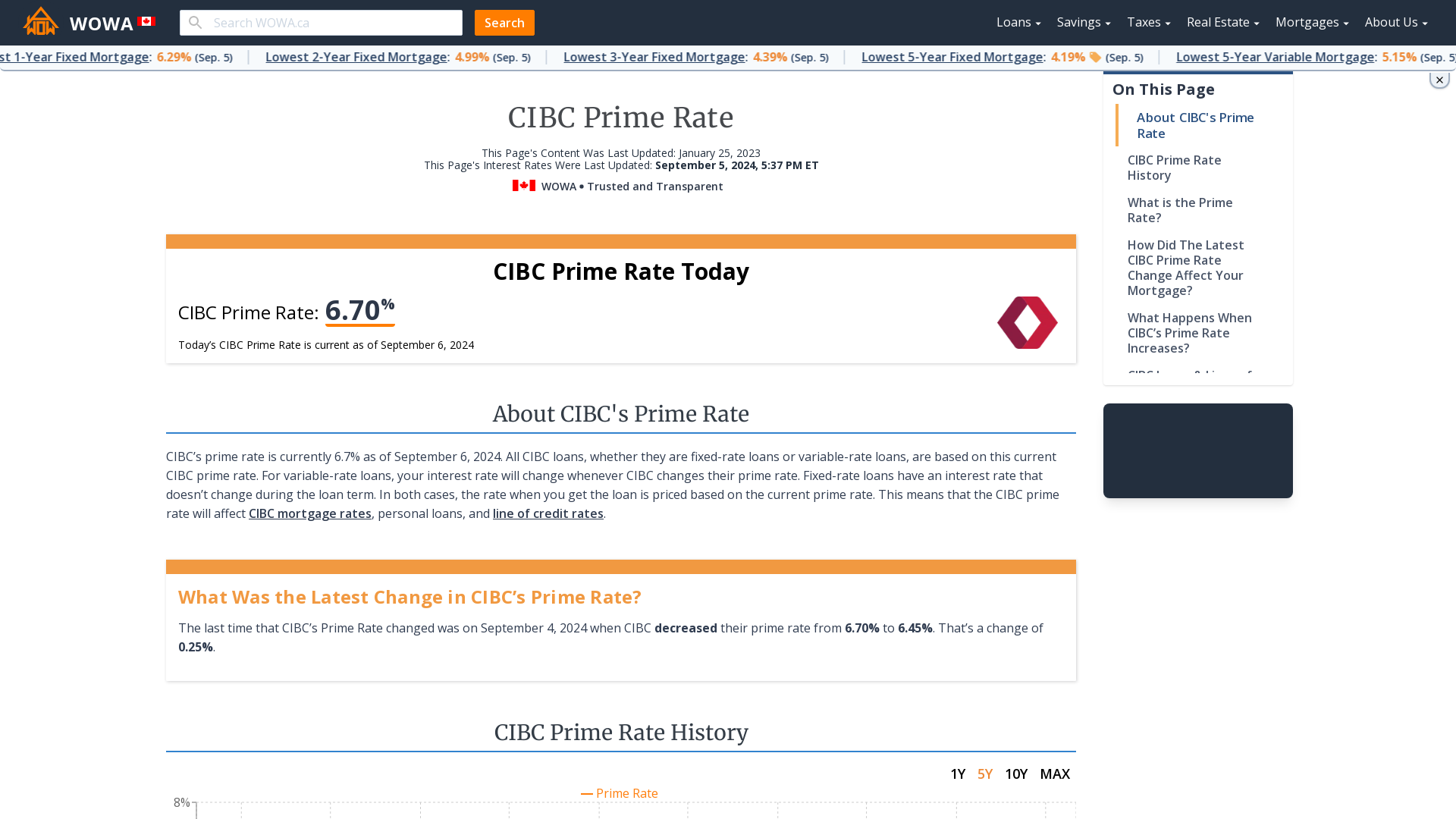

Adjustable-rate mortgage loans (ARMs) can help to save individuals a king’s ransom inside the interest rates more than the brand new brief so you can medium term. But when you was holding that when it is time for the newest interest rate in order to reset, it is possible to face a higher month-to-month home loan bill. That is great if you can pay for they, but if you are like a lot of the Us citizens, a boost in extent you pay monthly is probable are hard to swallow.

What exactly is an adjustable Rates Mortgage?

Think about this: Brand new resetting off changeable-price mortgage loans during the financial crisis shows you why, partly, a lot of people were pushed to your foreclosures otherwise must promote their homes basically transformation. Adopting the property meltdown, many monetary coordinators placed changeable-speed mortgage loans in the risky category. Just like the Arm has gotten a bum hiphop, it is really not a bad mortgage tool, provided consumers know what he could be entering and is upgrade a legitimate loan company you will what goes on whenever a changeable-rate home loan resets.

Trick Takeaways

- A variable-rates financial (ARM) is a kind of financial the spot where the interest used into the equilibrium varies about lifetime of the mortgage.

- Whenever rates rise, Arm borrowers can expect to invest high month-to-month home loan repayments.

- The latest Arm interest rate resets for the a beneficial pre-place agenda, often annual otherwise partial-a-year.

- With variable-rate financial hats, discover constraints seriously interested in exactly how much the eye pricing and you will/or payments can increase annually or higher new lifetime of the loan.

Interest Alter having an arm

Getting a grasp on what is within store to you personally with an adjustable-speed mortgage, you initially need to know how the item functions. With a supply, borrowers secure mortgage, always a decreased that, having a set time frame. Whenever that point frame stops, the mortgage interest resets to regardless of the prevalent rate of interest is actually. The first several months where in actuality the rate doesn’t transform selections anywhere away from 6 months so you’re able to ten years, according to Federal Financial Mortgage Business, or Freddie Mac computer. For almost all Arm activities, the speed a borrower will pay (plus the amount of the fresh new payment per month) can increase substantially after from the loan.

Of the initial low interest, it may be popular with borrowers, such as individuals who do not propose to stay static in their houses having a long time or that experienced sufficient to re-finance when the notice pricing go up. Lately, with interest rates hovering from the listing downs, individuals who had an adjustable-price home loan reset or adjusted don’t discover too-big a reversal within monthly installments. However, that could transform depending on how much and just how rapidly the brand new Government Set-aside introduces its benchmark rates.

Learn Their Improvement Period

In order to determine whether a supply is a good fit, individuals have to know some rules in the these finance. In essence, the brand new improvement period ‘s the period between interest changes. Need, for instance, a changeable-rate mortgage who’s got an adjustment age 12 months. The loan equipment would be titled a 1-year Arm, in addition to interest-and therefore the fresh month-to-month mortgage payment-do alter shortly after every year. Whether your modifications period try three-years, its named good 3-season Case, and speed create changes all of the three-years.

There are even some hybrid items like the 5/12 months Sleeve, which provides you a fixed price into the very first five years, and then the speed adjusts once from year to year.

Comprehend the Cause for the speed Changes

Along with understanding how commonly the Arm usually adjust, borrowers need to see the reason behind the alteration from the interest. Lenders ft Case cost to the certain spiders, with the most common as the one-season lingering-readiness Treasury securities, the cost of Fund Directory, in addition to prime price. Before taking away an arm, make sure you query the lender and therefore index would be put and you can evaluate the way it possess fluctuated previously.

One of the biggest risks Case individuals face when its loan changes is fee surprise in the event the monthly mortgage payment increases drastically by the rate changes. This will end in difficulty for the borrower’s region when they can not afford to make this new payment.

To end sticker surprise of happening to you, definitely stick to better interesting cost since your improvement months approaches. According to the User Economic Protection Panel (CFPB), mortgage servicers must give you an estimate of your own the newest fee. In the event the Case try resetting for the first time, you to imagine is sent to you eight to 8 days until the modifications. In the event your financing provides adjusted in advance of, you’ll be informed two to four months in advance.

Furthermore, towards the very first notification, loan providers should provide options that one can discuss if you fail to afford the the brand new price, and additionally information about how to contact a good HUD-acknowledged homes therapist. Knowing ahead of time precisely what the the latest percentage is just about to become will give you time for you cover they, check around for a much better mortgage, or rating assist determining what your choices are.

The conclusion

Trying out a changeable-rate home loan need not be a dangerous process, so long as you know what happens when their home loan interest rate resets. As opposed to fixed mortgages the place you pay the same interest more than living of your own financing, which have an arm, the rate vary after a period of time, and in some cases, it may rise somewhat. Understanding ahead just how much a whole lot more you are able to owe-or could possibly get owe-each month can possibly prevent sticker surprise. More significant, it helps always are able to help make your mortgage repayment each month.